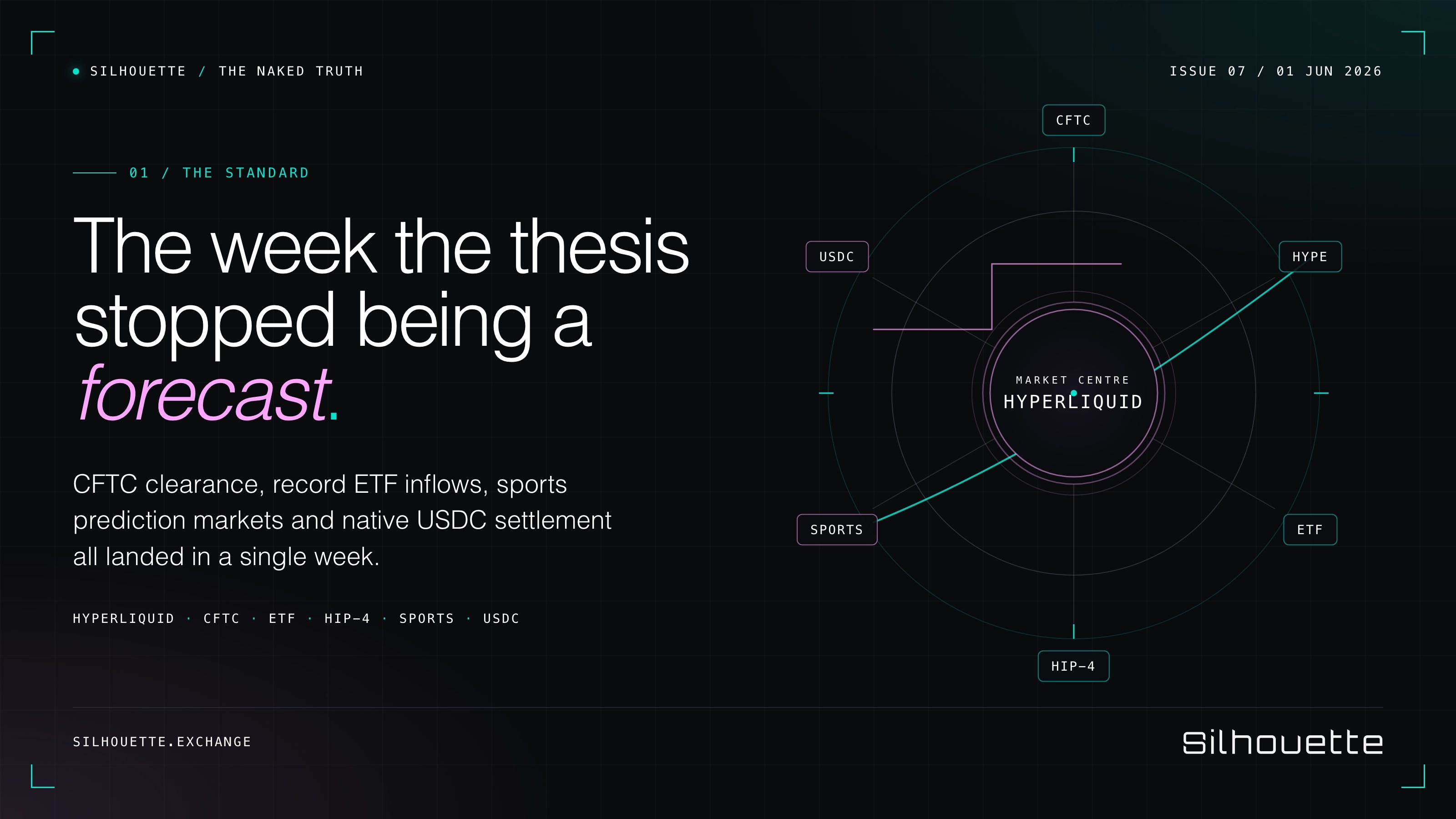

Hyperliquid - The Week the Thesis Stopped Being a Forecast

The Naked Truth · Issue #7 · A weekly read on what’s happening inside Hyperliquid’s ecosystem.

Welcome back. Last week the venue trade became the conviction trade. This week the capital and the products turned up to back the conviction.

You could trade the NBA Finals on Hyperliquid this week. On the same morning, an asset manager bought twenty million dollars of HYPE in a single session. Those two facts sit at opposite ends of one story, and the story is that the speculation about whether onchain venues can hold real financial activity is over. The activity is here. It is being measured in records.

Lead Story

The rails got cover, and the capital moved

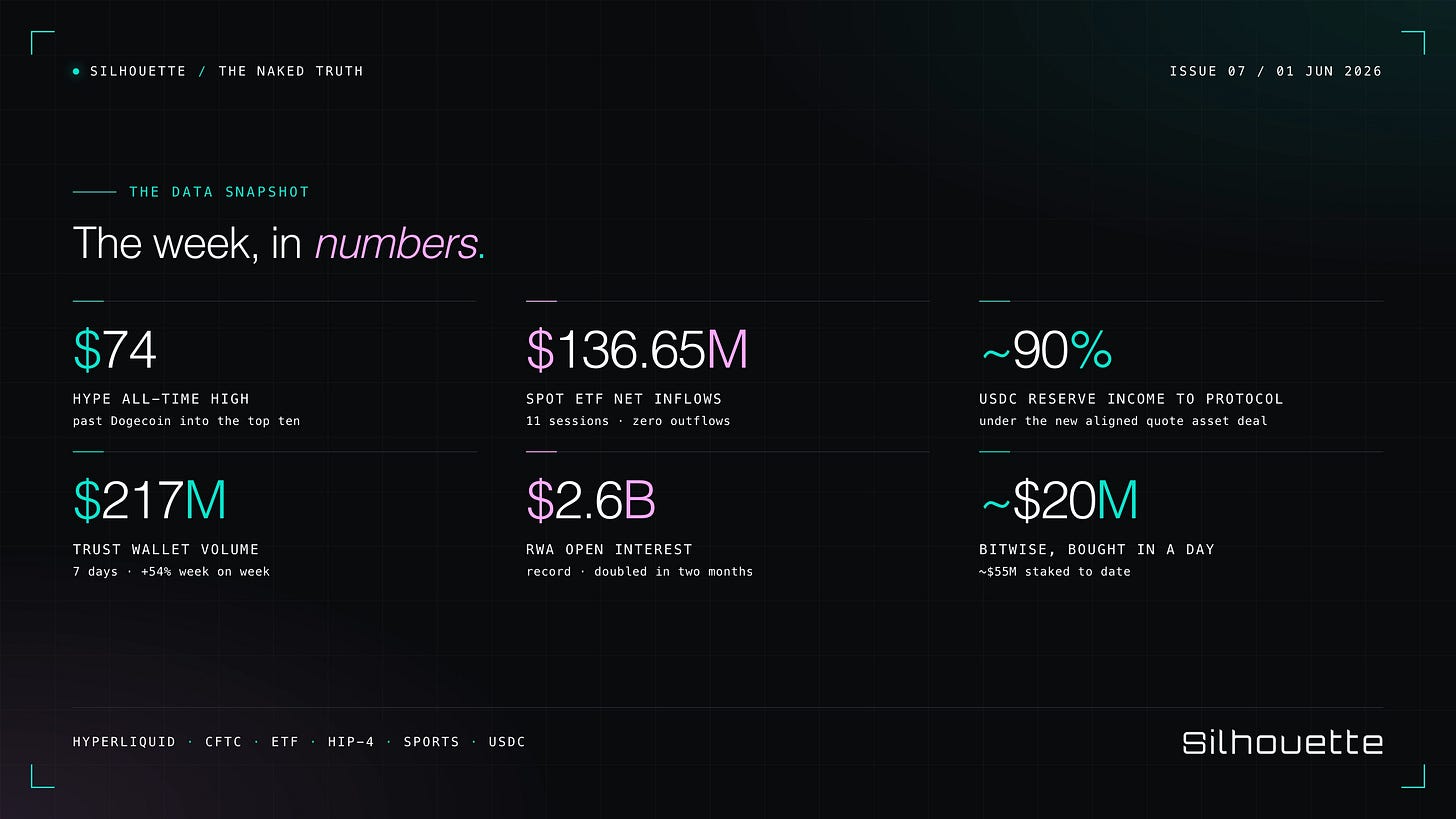

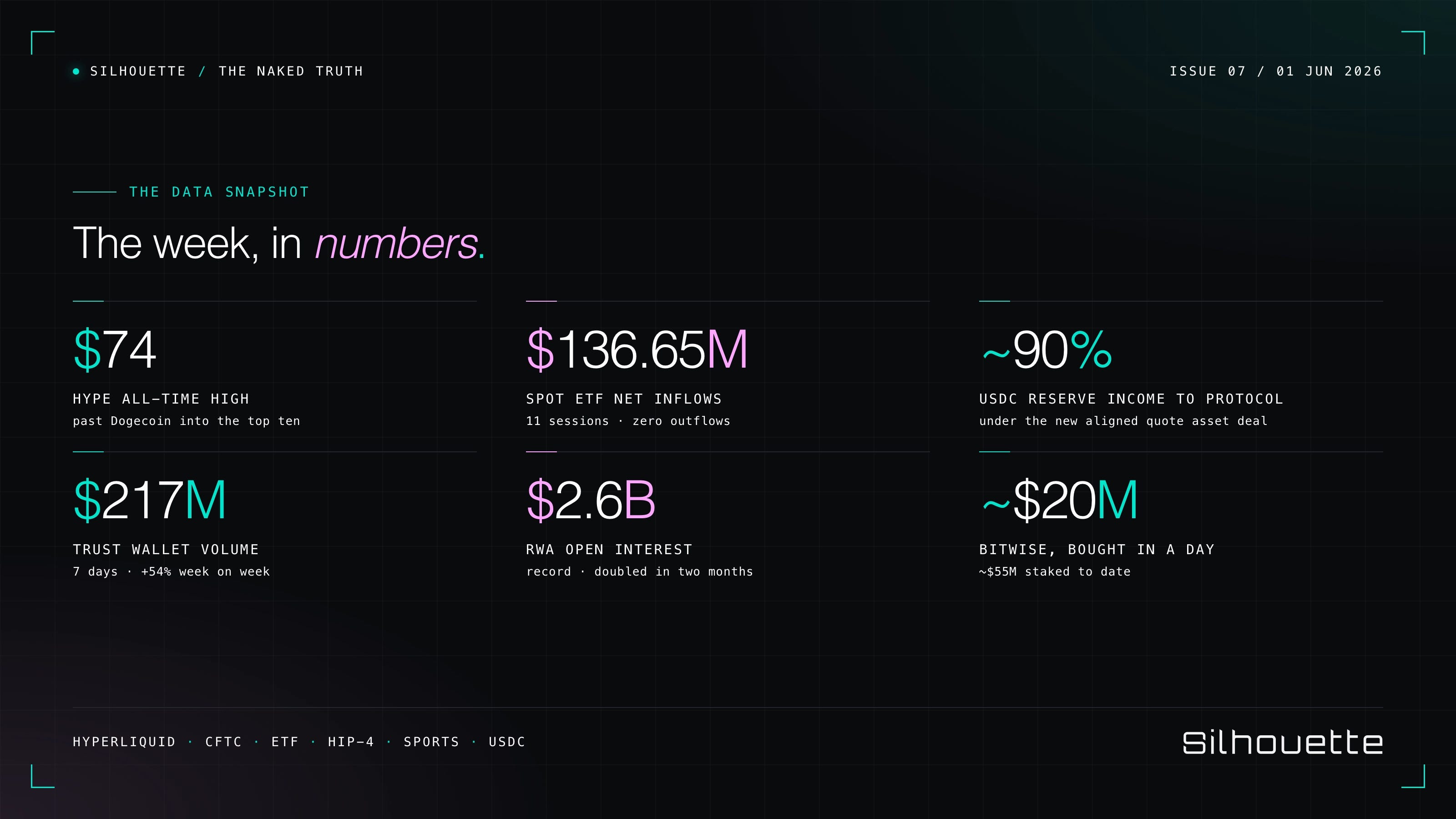

On 28 May the CFTC cleared perpetual futures at a regulated United States venue, opening a category that had lived offshore for a decade. Hyperliquid was not named in the ruling. It did not need to be. The market read the decision as validation of the product it already dominates, and it repriced accordingly. HYPE printed a record near seventy-three dollars by 1 June, pushing past Dogecoin into the top ten by market value.

The flows underneath the price are the part worth watching. United States spot HYPE products have absorbed roughly one hundred and thirty-six million dollars across eleven trading sessions with no outflows, the strongest altcoin fund debut of the year. Bitwise alone bought around twenty million dollars in a single day and has staked more than fifty million. Grayscale filed for its own spot product and accumulated half a million tokens in a week. This is not retail momentum chasing a chart. It is balance sheets taking position in an asset they have decided behaves like infrastructure.

The honest caveat belongs here too. The regulatory approval went to a competing venue and to a custodian, not to Hyperliquid directly, and a record set on inflows is a record exposed to outflows. The thesis is being confirmed, not completed.

Ecosystem Pulse

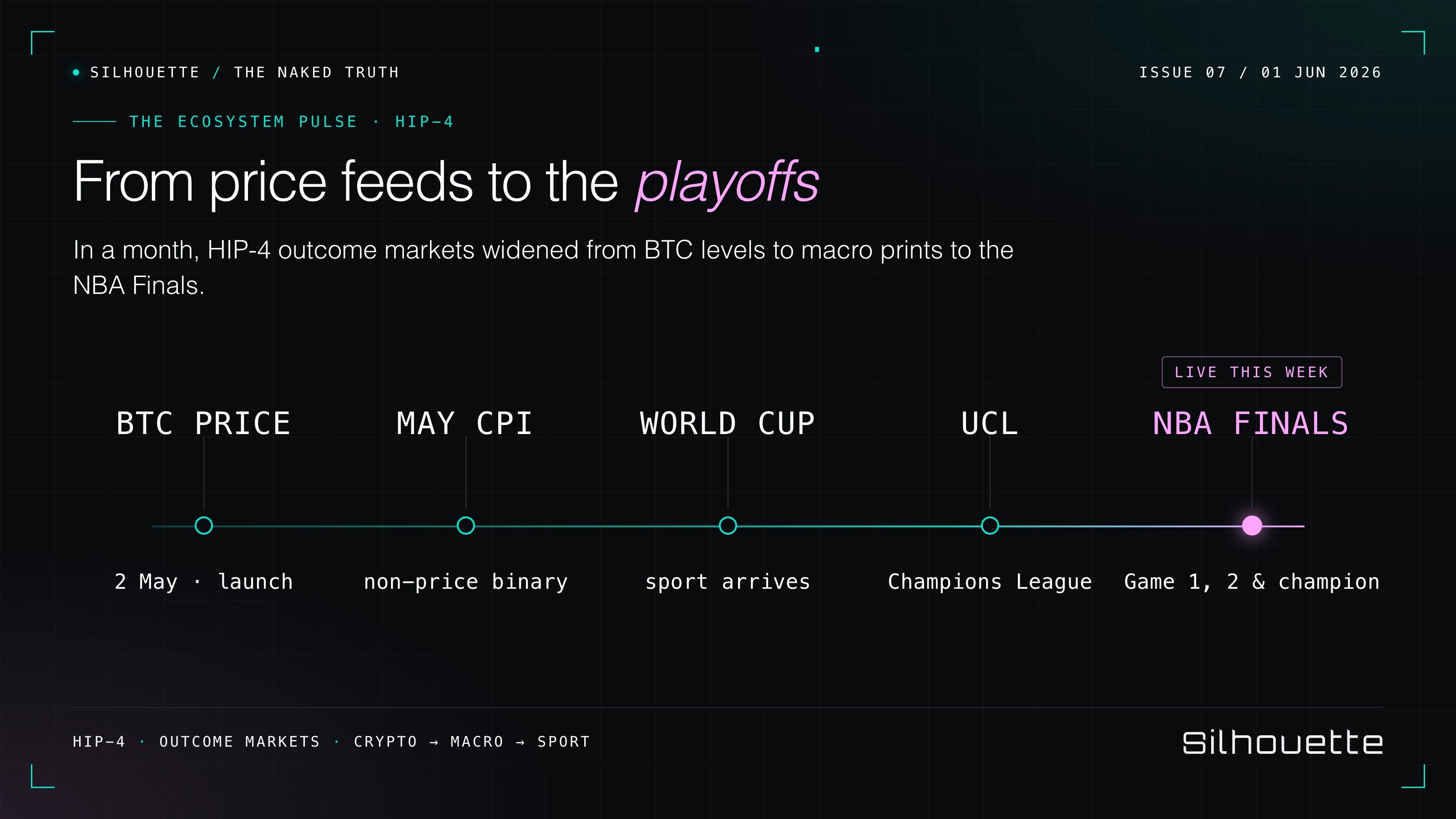

Prediction markets walked onto the court. Outcome launched NBA Finals markets on Hyperliquid this week, covering individual games and the championship, following World Cup and Champions League markets the week before. HIP-4 is steering toward sport, and sport is where the largest non-crypto audiences already understand the product.

A major wallet put outcomes in everyone’s pocket. Trust Wallet became the largest consumer wallet to embed Hyperliquid-powered prediction markets, placing perpetuals and outcome trading inside one self-custody app. It reported two hundred and seventeen million dollars of Hyperliquid volume in seven days, up fifty-four per cent week on week.

USDC moved to the centre of the stack. Under the new aligned quote asset framework, validator-operated HIP-4 and perpetual markets will quote in USDC, with Circle handling mint and cross-chain rails and Coinbase seated as treasury deployer. The protocol keeps as much as ninety per cent of the reserve income on those deposits, turning a stablecoin integration into a revenue line.

HIP-3 crossed a quarter of a trillion. Per ecosystem trackers, cumulative volume across all HIP-3 markets surpassed two hundred and seventy-five billion dollars, and tokenised stocks are now a growing share of total venue volume.

Real world assets set a record. Open interest in onchain real world assets reached an all-time high of two point six billion dollars, double the figure from two months earlier.

Data Snapshot

HYPE record high near $74, now a top ten asset by market value, ahead of Dogecoin

US spot HYPE products: ~$136.65M net inflows across 11 sessions, zero outflows

Bitwise: ~$20M bought in one session, ~$55M staked

HIP-3 cumulative volume: >$275B, per ecosystem trackers

HIP-4 outcome markets: live since 2 May, ~$100M cumulative volume (ecosystem trackers)

Real world asset open interest: $2.6B record, double two months prior

Trust Wallet Hyperliquid volume: $217M in 7 days, +54% week on week

Scheduled token release on 6 June: 9.92M HYPE, ~2.54% of supply

May CPI outcome market settles 10 June on official Bureau of Labor Statistics data

The Naked Take

The Bar Moved and It Is Not Moving Back

There is a line going round the timeline this week that captures the mood better than any chart. One builder put it plainly: Hyperliquid did the most damage to capital-C Crypto, because it set the standard so high that every team without a real product got exposed. He called it the era of get-good crypto. He is right, and the discomfort in that sentence is the point.

For years the industry rewarded the promise. A token launched, attention arrived, a narrative formed, and the product was something you would ship later, once the treasury was full. Hyperliquid inverted the order. It built a venue that generated revenue, distributed nearly a third of its supply to the people who actually used it, took no outside private rounds, and let the asset capture the value the protocol produced. The price followed the cash, not the other way round.

That is why the comparison everyone reached for this week, HYPE against Solana, misses what is actually being argued. The interesting question is not which token has the larger market value. It is which model survives contact with institutions that read income statements. When an asset manager buys twenty million in a day, it is not buying a story about decentralisation. It is buying fee generation, buybacks funded by usage, and a supply schedule it can underwrite.

The risk is the same shape as the strength. A standard set this high invites everyone to copy it, and most of the copies will fail in public, loudly, taking retail capital with them. A founder said it bluntly this week: if you are sidelined and thinking about running the Hyperliquid playbook, do not, because it will not work for you. The playbook is not a template. It is the residue of having built something people needed before anyone was watching.

So treat the records with the respect they deserve and the suspicion they earn. The capital that arrived this week can leave. The unlock on 6 June is real supply meeting real demand. But the thing that cannot be unwound is the standard. The market now has a working example of a crypto asset priced like a business, and once that example exists, the promise alone stops being enough. That is the genuinely durable change, and it is bigger than any single week of green candles.

Shield Report

The same flows that made this a record week are the reason shielded execution stops being optional. When balance sheets take positions measured in tens of millions, the venue stops being a crowd of anonymous retail orders and starts being a place where intent is legible. Size leaves a footprint. A large order worked in the open tells everyone watching what you are doing before you have finished doing it, and the better the venue’s data tooling becomes, the truer that gets.

Silhouette exists for the part of the market that is now arriving. As institutional size moves onto Hyperliquid, the ability to execute a block without broadcasting it first is the difference between a fill at your price and a fill at everyone else’s. The records this week are a demand signal. They are also a reminder that the bigger you trade, the more you have to protect how you trade.

Trade shielded at app.silhouette.exchange.

The Close

Two dates frame the week ahead. On 6 June a scheduled token release puts fresh supply into a market running hot, the cleanest test yet of whether usage-funded buybacks can absorb what conviction cannot. On 10 June the May inflation print settles the inaugural validator-resolved outcome market, the moment Hyperliquid’s prediction layer either proves its settlement design or finds its edge cases. Sport keeps pulling new audiences toward the product, institutions keep adding to positions, and the standard keeps rising for everyone who is not Hyperliquid. Watch the inflows, respect the unlock, and keep your own size to yourself.

Trade shielded.

The Naked Truth is published weekly by the team at Silhouette, shielded trading on Hyperliquid.

app.silhouette.exchange · @silhouette_ex · Telegram · Docs

Between massive call options volume spiking (running at 4x normal levels) and the fact that $PURR was recently confirmed for inclusion in both the Russell 3000 and Russell Microcap Index (effective later this month on June 26), passive index funds are going to be forced to buy up a ton of float. Combined with recent 13F disclosures showing heavy institutional accumulation from firms like Goldman Sachs, BlackRock, and State Street, the available liquid float "in the box" for market makers to short or hedge with is drying up rapidly.